An asset management firm’s ESG policy should rest on three pillars: a clear sense of purpose, a demarcation of the limits of materiality, and a strong connection to the investment proposition of the firm.

In this post, I look at the first of these: purpose.

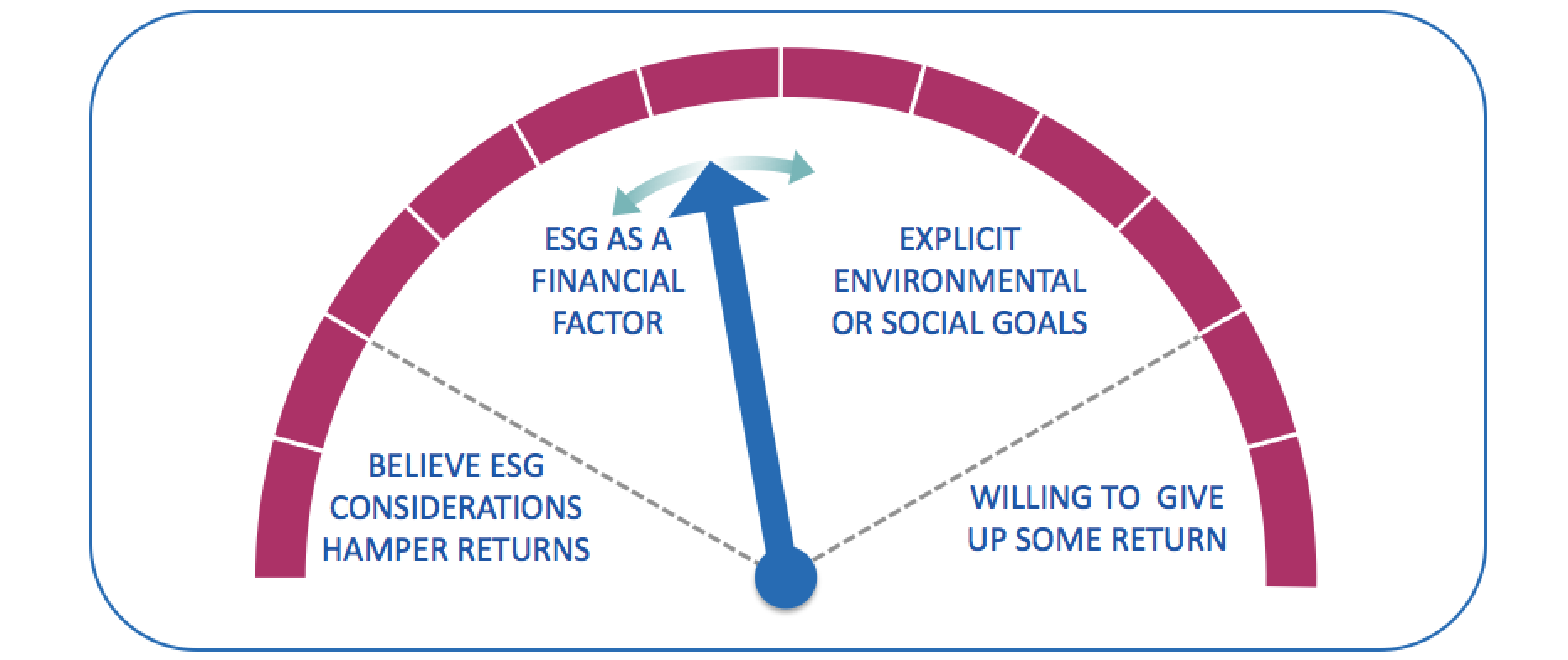

I will do so using a tool that we call the impactometer. As the (admittedly ugly) name implies, this is a gauge of the extent to which ESG considerations drive investment decisions. It covers the spectrum from antagonism to unconditional embrace, a spectrum that we might think of as running from Ayn Rand to Greta Thunberg.

Ayn Rand – who is cited as a formative influence by many political and economic leaders – dismissed environmentalism as nothing more than a front. In her opinion, “the immediate goal is obvious: the destruction of the remnants of capitalism… and the establishment of a global dictatorship.” She argued that preindustrial life expectancy was 30 years and, accordingly, instructed anyone older than that to “give a silent ‘Thank you’ to the nearest, grimiest, sootiest smokestacks you can find.”

Greta Thunberg, of course, takes a different view: “I want you to panic… I want you to act as you would in a crisis. I want you to act as if our house is on fire.”

If these positions represent the ends of our spectrum, there is a lot of room in the space between, where most ESG policies lie. (In an appendix this post, I provide a few other quotations pertinent to the issues at play here).

There are two primary determinants of where a firm sits: the prominence of ESG factors in the investment decision-making process, and the willingness to see environmental and social outcomes as desirable objectives in their own right.

From 0 to 60

In the diagram above, a position below the dashed line on the left of the chart would indicate that ESG considerations are presumed to conflict with financial goals, and that they tend to destroy value.

Today, almost every investment organization says that it takes ESG factors into account in investment decisions when those factors are judged to be financially material. But that statement alone does not tell us whether in practice that happens frequently, occasionally, or hardly at all. Hence, as we move up the left hand side of the impactometer, ESG considerations become a growing component of financial analysis. Because ESG factors typically emerge over time, there is a connection here to the time horizon of the investment process.

Moving past the top of the dial indicates that ESG considerations are regarded not only as financial factors but also as valid goals in their own right. Although some would assert that any attention paid to environmental or social goals must necessarily compromise the focus on financial return, there is a case to be made (as, for example, I have done in a previous post) that scope does in practice exist. Moving along the right hand side of the dial represents an increasing emphasis of these ESG goals.

While the scope to pursue environmental or social goals without compromising financial objectives does exist, it is not unlimited. At some point, the goals will conflict. Passing the dashed line on the right of the chart indicates a willingness to sacrifice financial benefit in order to achieve social or environmental goals.

Using the impactometer to reach a common stance

It would be a highly unusual asset management organization where everybody prefers the same position on the spectrum described above. Without an explicit dialogue, differences of opinion are sure to exist both about where the firm actually sits, and about where it ought to sit. It is worth bringing those differences out.

A firm should be willing to take ownership of wherever it sits on the impactometer spectrum. A firm must believe in its process. If ESG risks are treated as minor considerations that are supplementary to other factors seen as more financially significant, then the firm does itself and its clients no favors if it spins a different story for marketing purposes. The same applies to one’s attitude to non-financial objectives. The firm’s position should be known, accepted and applied across the organization.

Where do firms sit?

The graphic below places 40 asset management organizations on the impactometer spectrum, based on my own (completely subjective) reading of their investment policies, ESG policies, PRI transparency reports, and other public materials. In some cases, the signals were rather mixed. I should also note that the firms shown here are a biased sample of the asset manager universe: large firms are over-represented, as are those with strong ESG reputations.

We see that none of the organizations I looked at describe ESG factors as detrimental to returns. Similarly, even though some pursue non-financial objectives, this is done alongside rather than at the expense of financial goals.

Most firms pursue purely financial objectives. Indeed, it is likely that firms pursuing non-financial objectives are over-represented in the group sampled. The prominence of ESG factors within the investment process, however, varies.

A clear sense of purpose means knowing where the firm sits on the impactometer spectrum, and embracing that position. This is the first of the three pillars on which ESG policy rests. In upcoming posts, I will turn to the other two: materiality and the connection to the firm’s investment proposition.

More information on the ESG beliefs exercise can be found here.

The impactometer in quotes

“Anyone over 30 years of age today, give a silent ‘Thank you’ to the nearest, grimiest, sootiest smokestacks you can find.”

Ayn Rand. Return of the Primitive: The Anti-Industrial Revolution.

“Fiduciaries must not too readily treat ESG factors as economically relevant.”

The US Department of Labor. Field Assistance Bulletin 2018-01.

“The social responsibility of business is to increase its profits.”

Milton Friedman. The New York Times Magazine.

“The business case for ESG investing is empirically very well founded.”

Gunnar Friede, Timo Busch & Alexander Bassen. ESG and Financial Performance: Aggregated Evidence from more than 2000 Empirical Studies. (in the Journal of Sustainable Finance & Investment)

“Companies that pay most of their attention to the bottom line will fail.”

George Russell. Success by Ten.

“Any institution exists for the sake of society and within a community. It, therefore, as to have impacts; and one is responsible for one’s impacts.”

Peter Drucker. Management: Tasks, Responsibilities, Practices.

“We aim to ensure our impact avoids negative impacts on the environmental, social and financial systems, and, preferably, promotes positive impact as well as private financial reward.”

James Hawley & Jon Lukomnik. An Asset Management Hippocratic Oath (in The Purpose of Asset Management)

“Investment and fiduciary duty has always been a three dimensional problem of risk, return and impact.”

Thinking Ahead Institute. Mission Critical: Understanding Value Creation

“I want you to act is if the house is on fire.”

Greta Thunberg. Speech to World Economic Forum